The interest rate that moves markets is the federal funds rate. Also known as the discount rate, the rate depository institutions are charged for borrowing money from Federal Reserve banks.

The federal funds rate is used by the Federal Reserve (the Fed) to attempt to control inflation. By increasing the federal funds rate, the Fed attempts to shrink the supply of money available for purchasing or doing things, thus making money more expensive to obtain. Conversely, when it decreases the federal funds rate, it increases the money supply and encourages spending by making it cheaper to borrow. Other countries’ central banks do the same thing for the same reason.

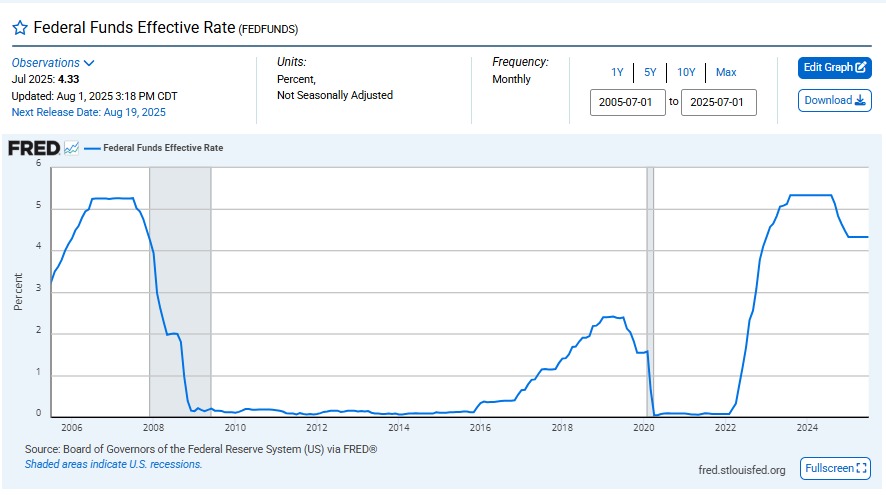

Below is a chart from the Fed showing fluctuations in the federal funds rate over the past 20 years:

Why is this number, what one bank pays to another is so significant? Because the prime interest rate—the interest rate commercial banks charge their most credit-worthy customers—is largely based on the federal funds rate.

It also forms the basis for mortgage loan rates, credit card annual percentage rates (APRs), and a host of other consumer and business loan rates.